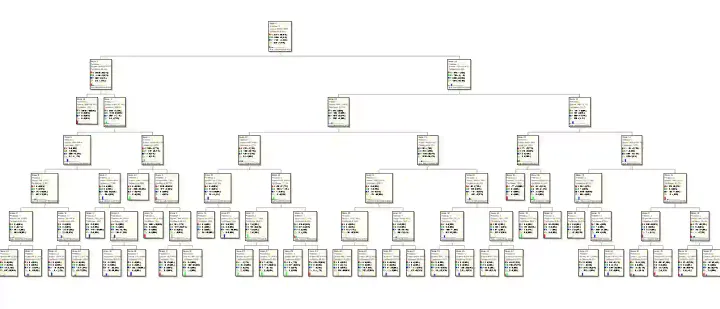

Boost Debt Collection and Recovery using Machine Learning [part 2/5]

In response to readers' demand, we've published a thorough and insightful real-world case study on Gumroad. This is an end-to-end machine learning case study that will assist you in increasing debt recovery by improving the traditional debt collection system of your crediting company.

![Boost Debt Collection and Recovery using Machine Learning [part 2/5]](/content/images/size/w1200/2024/05/debt_recovery_using_machine_learning-1.webp)